Shutdown Continues to Limit Economic Data

Key Takeaways

- Major banks reflect on economic resilience in earnings reports.

- Small-cap stock returns catching up to large-caps.

- Corporate earnings expected to show increases as companies report third quarter results.

With the ongoing U.S. government shutdown there continues to be virtually no economic data being released. Despite the scarcity of official government statistics there are other sources available to help discern the health of the U.S. economy. One of these sources is the commentary that accompanied the release of third quarter earnings reports from some of the nation’s largest banks. In aggregate, as reported in the Wall Street Journal, the nation’s six largest banks reported a year-over-year increase in their earnings of 19%. In the comments made in conjunction with their earnings releases, it was referenced that consumers continue to spend at a healthy rate demonstrating an ongoing resilience. These reports also included some concerns about ongoing geopolitical uncertainty and the previously referenced government shutdown.

Additional insight into the U.S. economy was provided by the release of the Federal Reserve’s Beige Book. This report provides anecdotal information regarding current economic conditions across the Fed’s 12 districts. In the edition released this week, it was reported that demand for labor remains muted, and all 12 regions were experiencing price increases. Despite the increase in prices, it is anticipated that the Fed will reduce the Fed Funds rate at its meeting later this month.

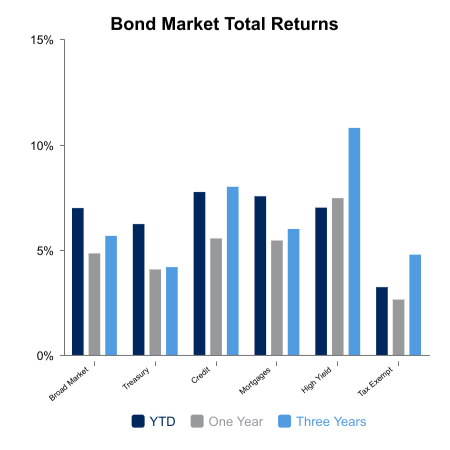

Turning to financial markets, performance was mixed as fixed income returns were positive while equities were slightly negative. Bonds benefited from a decline in interest rates as the 10-year U.S. Treasury issue saw its yield fall to 4.05% from the prior week’s level of 4.13%. The decline in yields translated into a 0.5% weekly return for the broader bond market. On a year-to-date basis aggregate bond indices have delivered a return of approximately 6.7%.

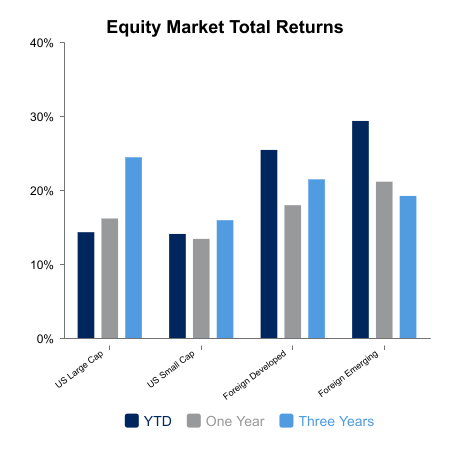

While the broadest measure of domestic equities had a return that was marginally negative for the week, the performance of the underlying components was vastly different. Small-cap stocks, as measured by the Russell 2000 Index, returned 2.5% and the Russell 1000 Index of large and mid-cap stocks delivered a return of -0.5%. With its recent strength small-cap stocks have moved into a virtual tie with the larger cap segments of the market with a year-to-date return of 14.2% versus the Russell 1000 Index return of 14.4%.

Over the next couple of weeks, the release of additional third quarter earnings reports will add further clarity to how the economy is performing as company leaders share what they are anticipating for the go-forward environment. According to FactSet, third quarter earnings for the S&P 500 Index are expected to show year-over-year growth of 8.0%.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.