Dealing with a Data Deficit

Key Takeaways

- Impact of government shutdown likely to be small on the economy.

- Fed likely to make a rate cut next week.

- Third quarter earnings reports are strong so far.

The U.S. government shutdown is now in its twenty-third day, making it the second longest in history. While the estimated impact on annualized GDP is between 0.1% and 0.2% for each week the shutdown continues, its long run impact on the economy may be modest. Forecasts of next week’s third quarter GDP release is estimated to show the economy grew 3.0%, down from 3.8% the previous quarter. If this momentum carries into the fourth quarter, the impact of the shutdown on the economy will look like a normal slowdown that is in line with current trends.

Tomorrow the Bureau of Labor Statistics releases its delayed September measure of the change in prices paid by consumers for goods and services, the Consumer Price Index (CPI). Economists estimate the 3.1% rate to be reported is a modest enough level to keep the Fed on track for further rate cuts. This CPI release was necessary to set the cost-of-living adjustment for next year’s Social Security payments.

Federal Reserve policymakers meet next week to decide if they should cut the Federal Funds Rate cut from 4.25% to 4.0%. For a committee that has emphasized data dependency, the lack of data has forced the Fed to pivot to private sector indicators and past data it has collected. Job indicators like the ISM employment data reflect a weaker jobs market, while sentiment surveys continue to show consumers are concerned about job availability and inflation.

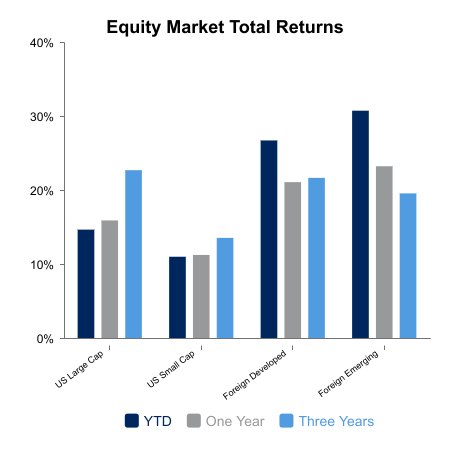

Third quarter consensus earnings growth for last quarter and the outlook through the end of 2026 remains positive, supporting profit margins. Around 12% of S&P 500 companies have released earnings with 86% of the companies beating expectations. So far this is one of the best starts to an earnings season in the last four years. Domestic equity markets as measured by the S&P 500 Index advanced 1.0% this week, bringing the year-to-date rise to 14.9%. The past month has seen leadership changes among economic sectors as health care and utilities have replaced technology focused sectors as the top performers. This shift of market leadership reflects a broadening of market leadership and economic participation of different sectors that form a diversified portfolio.

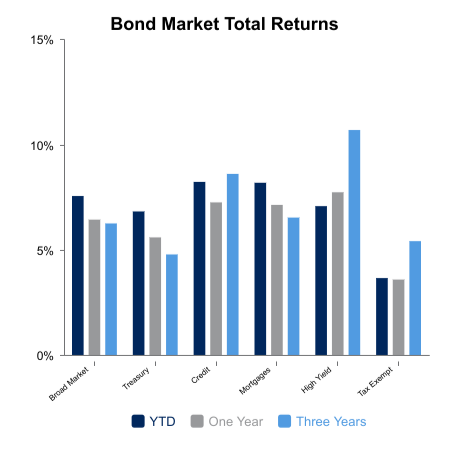

Bond markets inched ahead this past week by 0.2%, adding to the 1.3% return since quarter-end as yields across the curve have declined. Without new economic data, yields have continued to slip as markets continue to rely on an economic picture that reflected slowing growth. Lower rates helped boost home sales last month as the 30-year fixed rate dropped to 6.34%, its lowest level since 2022.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.