Equities moved higher this week as earnings take center stage. The S&P 500 advanced 0.5% and outpaced flat returns on the Bloomberg Barclays Aggregate Bond Index. The dollar has been soft as of late, which is giving a tailwind to higher beta assets and foreign equities. Foreign developed gained 0.9% on the week and emerging markets pushed up 0.7%. Small cap domestic equities fared the best of the bunch with a jump of 1.8%.

Building permits missed expectations on the month but remain up 8% on year-over-year basis. Housing continues to improve on the back of easier financial conditions coupled with a steady employment backdrop. The Conference Board Leading Economic Index was soft again, but the diffusion index remains okay at 55%. Regional manufacturing surveys are coming in decent and could signal some stability in the now closely watched ISM manufacturing survey. This is one of the primary indicators used to paint a downbeat view on future economic prospects. The market is hyper-sensitive to monthly changes in the ISM despite the series being quite noisy on a month-to-month basis. Still, stability in this indicator in early November could help put in motion an upward drift in risk assets into year-end as a repeat of last year fades from investor memories.

The Federal Open Market Committee (FOMC) started buying Treasury bills at a rate of $60 billion per month earlier this month. They made sure not to call it quantitative easing (QE) as this term has taken on a negative connotation. This week the FOMC upped the amount to $120 billion per month. The surge in budget deficits is forcing the FOMC to essentially monetize the debt in the guise of keeping markets orderly. The Federal Reserve asset base has increased 5% in the last five weeks, which is the same pace as the beginning of previous QE periods. The dollar has taken notice and fallen about 2% over the last month, but currency volatility remains exceptionally low by historical standards.

Mario Draghi just completed an eight-year stint as head of the European Central Bank. He never raised interest rates, but instead ushered in an era of negative interest rates. His replacement, Christine Lagarde, is touted as being more business and fiscal policy focused. This would be big news if true. A coordinated global fiscal initiative would have profound implications for various assets and as always markets will anticipate the outcome should early signs of traction emerge.

|

|

Contributed by | Justin Carley, CFA, Managing Director

Justin is a Managing Director, providing portfolio management and credit analysis for fixed income strategies. He also manages the firm’s multi-manager portfolio strategies and contributes to the asset allocation framework. Justin has more than 10 years of experience focusing on management, analysis and trading of fixed income portfolios. Previously, Justin was a fixed income portfolio manager at American Trust & Savings Bank. Justin has a bachelor’s degree from Truman State University, holds the Chartered Financial Analyst designation and holds a Fellowship in the Life Insurance Management Institute.

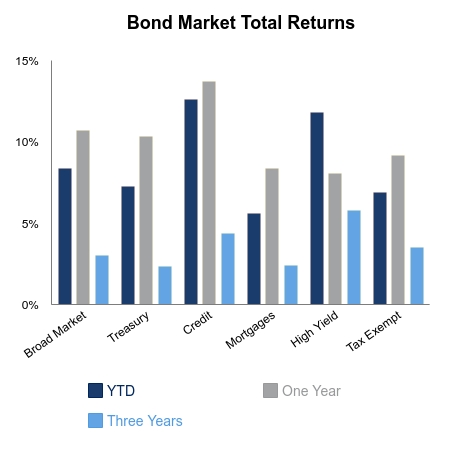

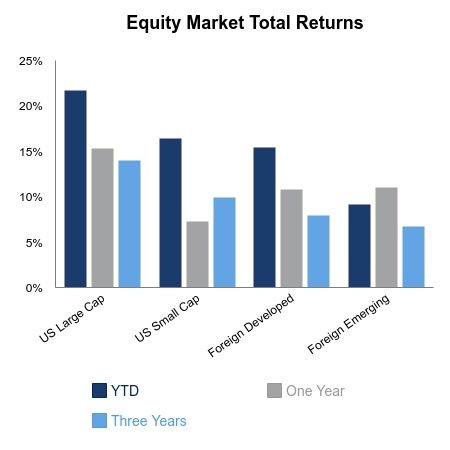

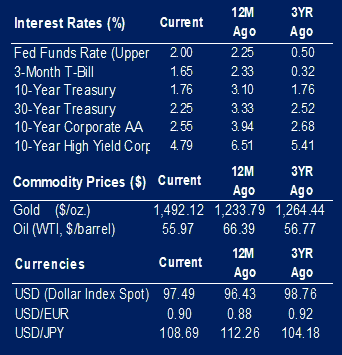

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.