Equities bounced back this week with domestic large caps outperforming small caps. The S&P 500 was up 1.2%, whereas small caps were flat. Bond yields inched higher resulting in little change in the Bloomberg Barclays Aggregate Bond Index. Emerging market and foreign developed equities underperformed in the United States.

Equities rallied sharply on Friday following a decent monthly jobs report where 136,000 net adds were reported. The economic data, especially manufacturing, has been quite soft and the market has become overly focused on near-term jobs related data. This causes a relief rally when the data doesn’t confirm a recession. Such was the case this week. Digging deeper into the numbers shows some softness underneath. The percentage of firms hiring over the last three months has fallen to its lowest level since 2010. At 56.8%, it remains above the red flag level of 50%. Job openings showed continued weakness and have contracted on a year-over-year basis for three consecutive months. The last time this happened was 2009. On the plus side, job cuts via the Challenger, Gray & Christmas report finally declined versus the prior year.

Prior to the equity rally, the ISM Non-manufacturing Index posted a large miss versus expectations. The index came in at 52.6 versus expectations of 55.0. This is suggestive that services, which has overwhelmingly held up the economy, may face a more difficult road going forward. Despite more data points continuing to suggest recession odds are increasing, some key variables say a different story. One measure is the Chemical Activity Barometer reported by the American Chemistry Council. It suggests the economy is not as weak as suggested by the ISM and other survey measures. Global leading indicators are also starting to get off the mat.

This week the United States is in trade talks with China. The market has been held hostage to every random headline. This was exhibited overnight where U.S. equity futures fell over 1% instantly, but then regained it all and rallied up 1% today on conflicting news headlines. It is likely we will get some knee-jerk market reaction to events prior to the Friday close. It is quite possible we are in a situation where the growing consensus forecasting a recession is wrong and the consensus call that a China deal will lead to a huge market rally is also wrong.

|

|

Contributed by | Justin Carley, CFA, Managing Director

Justin is a Managing Director, providing portfolio management and credit analysis for fixed income strategies. He also manages the firm’s multi-manager portfolio strategies and contributes to the asset allocation framework. Justin has more than 10 years of experience focusing on management, analysis and trading of fixed income portfolios. Previously, Justin was a fixed income portfolio manager at American Trust & Savings Bank. Justin has a bachelor’s degree from Truman State University, holds the Chartered Financial Analyst designation and holds a Fellowship in the Life Insurance Management Institute.

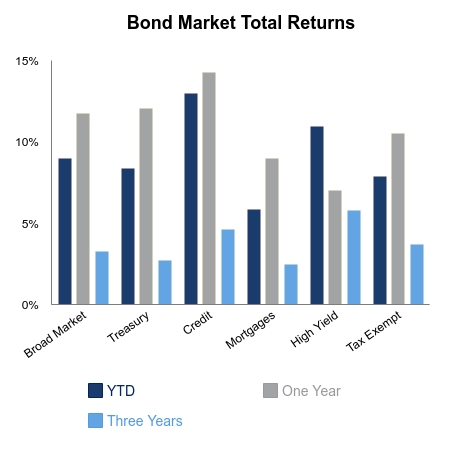

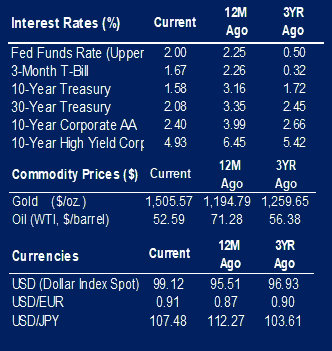

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.