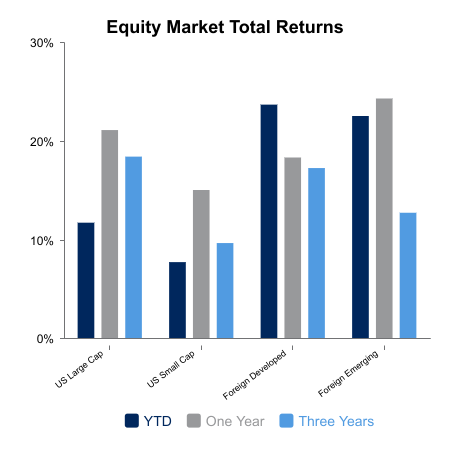

Financial markets treated investors quite well this week as both equities and bonds moved higher. In the U.S., both small cap and large cap equity indices delivered returns in excess of 1.0%. Mid cap stocks, as measured by the Russell Mid Cap Index were the laggards among domestic equities with a return of 0.7%. The strong one-week performance pushed the year-to-date return for the Russell 3000 Index of U.S. equities into double digit territory increasing from 9.9% last week, to the current result of 11.9%. As we approach the end of the third quarter, growth stocks are clearly in command versus their value counterparts as the Russell 3000 Growth Index has returned 7.5% quarter-to-date versus 3.9% for the Russell 3000 Value Index. International equities, as measured by the MSCI EAFE Index, also performed well returning 1.5% for the week.

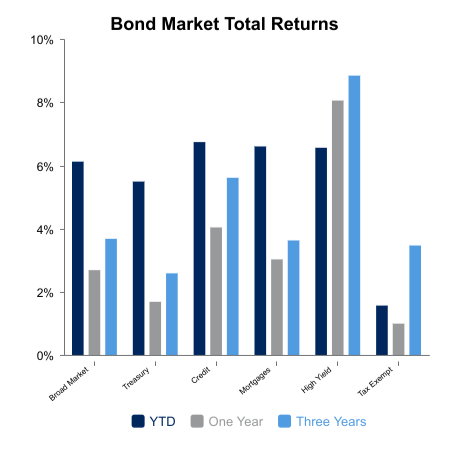

As referenced earlier, financial markets delivered strong weekly returns across the board last week, including fixed income. The weekly return for the broader bond market was 1.2% and the year-to-date return now stands at 6.3%. Driving the positive returns for bonds was a decline in interest rates as evidenced by the yield for the 10-year U.S. Treasury issue, which fell from a level of 4.22% at the beginning of the week to a yield of 4.04% at week’s end.

One of the primary drivers of the decline in rates was a weaker than anticipated employment report. The forecast for August non-farm payrolls was for an increase of 78,000 while the actual result was an increase of only 22,000. In addition, the report also revised down the results for the month of June to a decline of 13,000. Further enhancing the magnitude of this report was the release of revised job growth figures for the 12 months ending March 31. The announcement reported that there were 911,000 fewer jobs created over the one-year period than was previously estimated. The combination of these two reports has strengthened the probability the Federal Reserve will reduce the Fed Funds rate at its meeting next week. To quantify this potential move, CME Group’s FedWatch puts the probability of a cut at 100%. The methodology used to determine this probability also indicates additional rate reductions at the Fed’s October and December meetings.

On the equity front, with second quarter earnings virtually completed, the focus now turns to expectations for the third quarter. Currently FactSet estimates year-over-year quarterly earnings for the companies comprising the S&P 500 Index will increase 7.5%.

|

|

Sources: BTC Capital Management, BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.