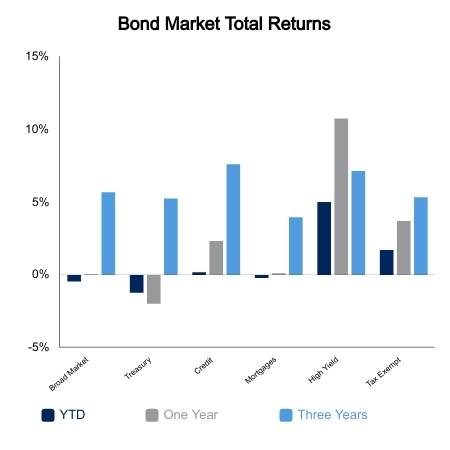

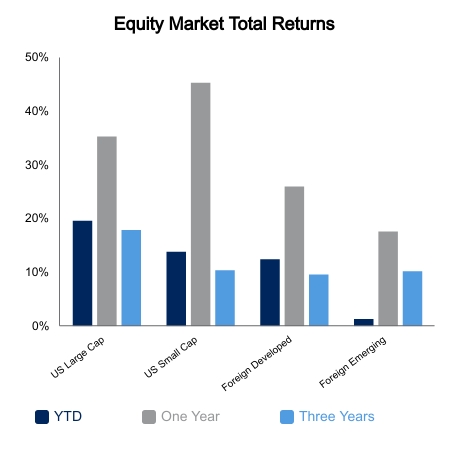

Equity markets slipped lower in the past week as early morning strength was consistently sold. Recently the Dow Jones Industry Average was down six out of seven days, but the magnitude was tame with just a 2.4% decline. Small caps have been the weakest area of the domestic market, falling 4.1% over the same span. Yields moved lower on the week, helping the Bloomberg Barclays Aggregate Bond Index advance 0.4% on the week.

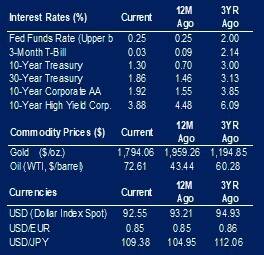

With inflation being a topic of concern, the Consumer Price Index (CPI) report was the highlight of the week. Both headline and core CPI came in lower than expected. Core CPI came in at 4.0% versus the prior year and is now lower for two consecutive months. The current backdrop is one of decelerating inflation, decelerating growth, and decelerating liquidity. These all may be temporary, and the causes are often debated, but until they reverse it remains difficult to see upward movement in Treasury yields.

It was a big week for economic data out of China with retail sales and industrial production missing forecasts by a wide margin. However, the more pressing point is what appears to be a commitment in China toward President’s Xi Jinping’s idea of a “common prosperity.” We have noted the fall in Chinese stocks as well as those listed in the United States. Las Vegas Sands and Wynn Resorts were each down more than 15% this week as crackdowns reach the gambling sector. Topping it all off is the fact that the second largest property developer, China Evergrande, stopped making bond payments today, as bankruptcy appears imminent. China Evergrande was larger than Lehman Brothers. The knock-on effects are still to be determined, but China’s largest property developer was down 20% this week on contagion fears.

Normally, the markets would be in a tailspin based on the facts at hand and enormous uncertainty. This has not transpired to this point as investors appear aware that everything rolls up to the sovereign and then China can handle the fallout. They just don’t appear willing to do so at this stage. While this could take a crash scenario off the table, China attempting to manage a deleveraging of their economy would certainly be a crushing blow to the reflation trade. It is likely that China’s policy responses in the coming weeks could be the primary determinant in setting the medium-term trajectory of markets.

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.