Equities sold off again this week, taking their cue from weakness that began during the Federal Open Market Committee (FOMC) press conference. The S&P 500 was down 4.4%, while emerging market equities fell 3.5%. Again, fixed income provided no hedge with the Bloomberg Barclays Aggregate Bond Index down fractionally. The NYSE Arca Gold Miners Index was down 11.9%. Since equities peaked early in the month, the S&P 500 has fallen 9.5%, the NASDAQ Composite is down 11.8%, and the MSCI Emerging Market Index has lost 3.6%. Reports of money laundering among large global banks put pressure on that group. The European Bank Index was down 12% on the week.

Initial jobless claims came in very close to consensus at +860,000. Continuing claims remain elevated as permanent job losses continue to move higher. Housing starts missed expectations, falling 5.1% on the month. Weather probably played a significant factor. Building permits were also softer than expected, but likely fell victim to similar weather dynamics. The Conference Board US Leading Economic Index was up 1.2% and continues to move in the right direction. Concerningly, the number of components in expansion fell from 80% to 50%. Flipping negative this month were manufacturers new orders and building permits.

The FOMC meeting last Wednesday appeared to make a stronger commitment to remaining accommodative until inflation is well over 2%. They added inflation expectations need to be anchored above 2% instead of just monthly inflation readings. This seemed like it could push equities up as they initially moved higher but selling began again during the FOMC press conference. Some analysts noted a less polished and less confident Chairman Powell. Equities seemed to sense this as well and have remained weak ever since. Adding to the weakness were a host of political events that will likely remain for some time. The decision over the Supreme Court seat vacated by Justice Ruth Bader Ginsburg brings into doubt whether more fiscal stimulus can be agreed upon. We have long since passed the original expiration and while everyone agrees more is needed, nobody appears willing to do anything. In this sense, it seems Congress is stalled until forced to act, i.e. the markets falling sufficiently far enough, or the Federal Reserve becomes much more proactive. Things are also more worrisome from a global growth standpoint as Europe hinted it was closer to imposing a second lockdown as virus counts increase.

|

|

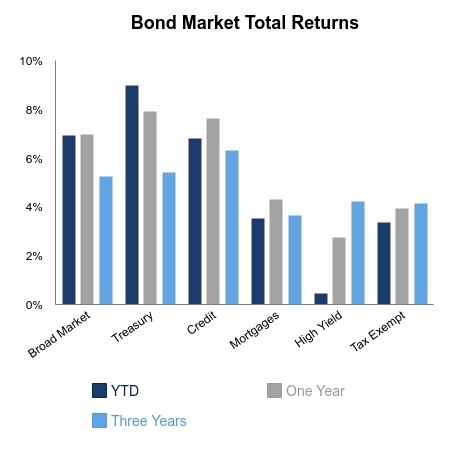

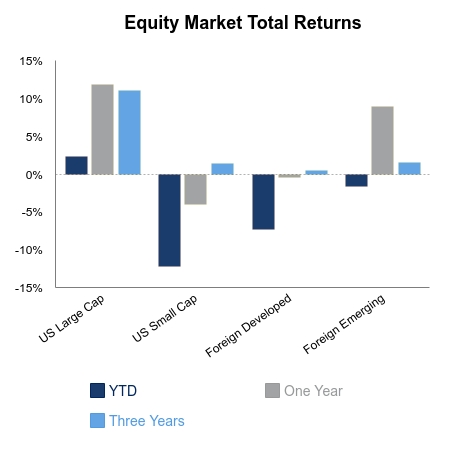

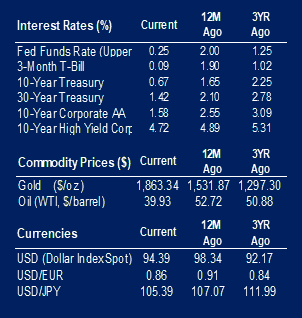

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.