Closing Out a Strong Third Quarter

Key Takeaways

- Global equity markets continue their year-to-date (YTD) rise.

- Economic indicators not too hot, not too cold.

- Going into the fourth quarter.

Global equity markets continue their YTD rise

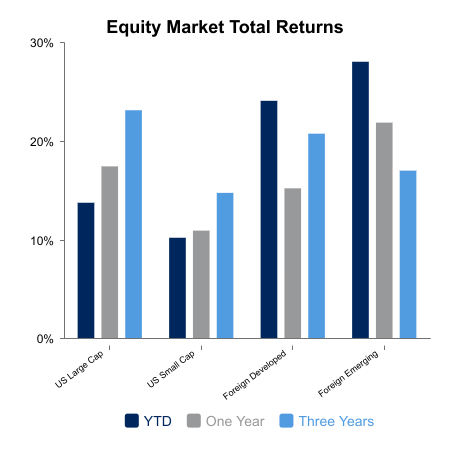

Over the last week, broad U.S. indices rose as the Russell 3000 Index increased 0.5%, the Russell 2000 Index rose 1.2% and the Russell 1000 Index returned 0.5%. Sentiment appears driven by a continuation of the AI‑trade, expectations for increasing corporate profitability, easing by the Fed, and a resilient consumer.

Outside the U.S., the MSCI All‑Country World Index ex‑USA (ACWI ex-USA) declined 0.2%, MSCI EAFE fell 0.6% while the MSCI Emerging Markets Index rose 0.3%.

YTD the Russell 3000 Index has risen 13.6% while ACWI ex-USA has surged 26.1%.

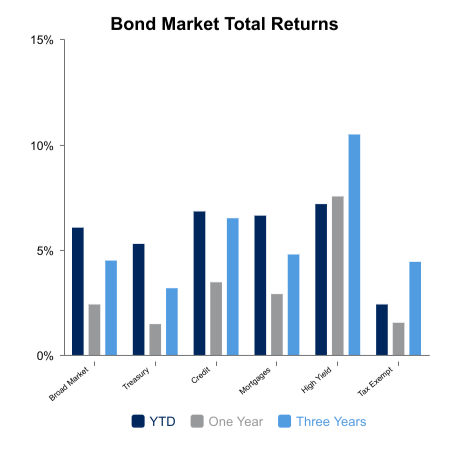

For the week, bonds retreated 0.4% given a near-term rise in interest rates since the Fed rate cut last week. For the year, bonds have returned 6.0%.

Economic indicators not too hot, not too cold

S&P Global released its flash PMI measures for September. Composite PMI came in at 53.6, Manufacturing PMI at 52.0, and Services PMI at 53.9. All reports were below both consensus and the prior month’s report but remain above 50 indicating expansion; below 50 indicates contraction. S&P noted U.S. business activity slowed for the second‑successive month due to declining demand. Growth was exhibited in both manufacturing and services, albeit slowing. Employment rose for the seventh-straight month.

New home sales for August advanced 20% to 800,000 units, a 3½-year high. July sales were revised up while the new housing inventory receded to an eight-month low. The Mortgage Bankers Association reported mortgage applications rose 0.6% week‑over‑week. Note that applications surged 30% last week after the Fed rate cut. Conversely, August building permits were revised down to 1,330,00 units, their lowest level since May 2020.

The final estimate of U.S. GDP comes out Thursday, as does durable goods orders and existing home sales, both for August.

Going into the fourth quarter

The U.S. is facing a prospective government shutdown as of September 30. Surprisingly, this is not the predominant search within Google Trends. More than two million searches have been accomplished for “Tylenol” and “Jimmy Kimmel return”; only 100,000 for “Government Shutdown 2025”.

Earnings reports for the third quarter will begin in earnest the week of October 13. Analysts appear optimistic projecting third quarter EPS growth of 13.5% year‑over‑year (YOY) for US companies. For foreign companies, analysts currently project EPS YOY growth of 10.0%. Stay tuned.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., London Stock Exchange Group Plc, FTSE Russell, S&P Global, Inc., US Census Bureau, Mortgage Bankers Association.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.