The S&P 500 Index was down 0.80% this week. There is concern supply chain issues may continue into next year leading to tighter margins. The spread of the Delta variant also contributed to downward pressure on the market this week. Reopening has been slower than expected, with some places reclosing and requiring vaccinations. Real Estate, Information Technology and Health Care sectors performed the worst this week while Energy, Financials and Industrials sectors performed the best.

There was another dip in consumer confidence in September after decreases in July and August. The index was at 109.3, lower than the previous month’s 115.2 and the expected 114.3. Consumer confidence was negatively impacted by the spread of the Delta variant. Concerns around inflation eased a bit in this report.

The supply situation for homes continued to improve in August. 740,000 new homes were sold. This is better than the expected 710,000 and the previous month’s 729,000. We had seen some declines in this number as supply failed to keep up with home demand in the first part of the year. The current median price of a new home is $390,900.

More building permits were issued in August than in the previous three months. Despite the growth, the reading of 1.721 million was lower than the expected 1.728 million.

The star in housing reports this week was pending home sales. The index jumped 8.1% in August even though expected growth was only 0.70% and the previous month saw a 2% decline. The sharp increase was attributed to increasing supply and flattening of prices. These trends in housing are expected to continue.

Trends in manufacturing have been positive in September. The Markit PMI Manufacturing index is at 60.5. The index is an indicator of the direction purchasing managers think the economy is going. The service PMI was a little weaker at 54.4 but still strong. The PMI composite was at 54.5. The Markit PMI indices are diffusion indices. Readings over 50 are considered positive.

Durable Orders were up 1.8% in August. Orders have been up 15 of the last 16 months. The largest contributor to growth was orders in transportation equipment.

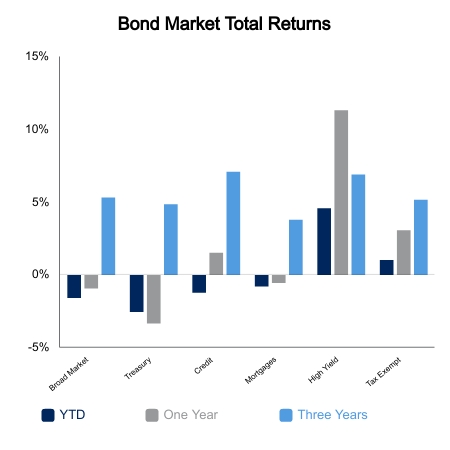

|

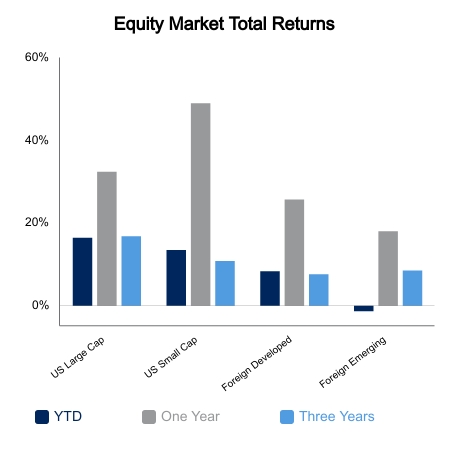

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.