A Great Month So Far

Key Takeaways

- Earning season is off to positive start.

- April recovery of equity markets.

- Retail sales are boosted by energy prices.

As first-quarter earnings season progresses, corporate guidance has highlighted robust U.S. consumer resilience, paired with a differentiated approach to managing elevated input costs, ranging from active price adjustments to wait-and-see monitoring. Early reporting indicates strong results for the S&P 500 Index, with an earnings-per-share (EPS) surprise of 8.2%, surpassing the historical average of 4.4%. Furthermore, revenue performance has been strong, with 62% of companies posting positive surprises. This represents an upside adjustment relative to analysts expectations, which were intentionally set in line with fourth-quarter figures in anticipation of slower Q1 economic growth.

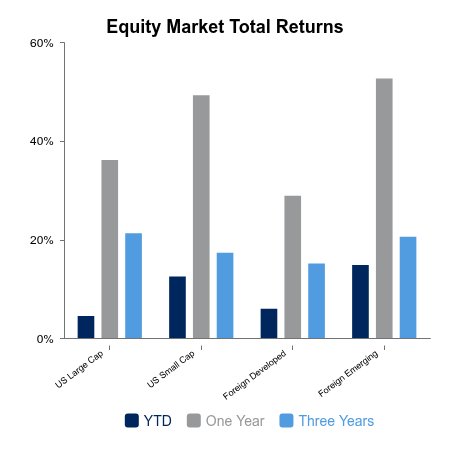

U.S. equity markets advanced 1.4% this week, extending the total April gain to 9.2%. If sustained, this would mark the strongest single-month performance since July 2022, a period also characterized by market recovery following headwinds from rising energy costs. Following this recovery rally, the Russell 1000 Index has advanced 4.6% year-to-date (YTD). Small cap stocks have shown significant momentum, appreciating 11.6% in April, bringing their YTD gain to 12.6%. International equities also rallied in response to diminishing geopolitical tensions in the Middle East, rising 9.8% for the month and 9.1% YTD.

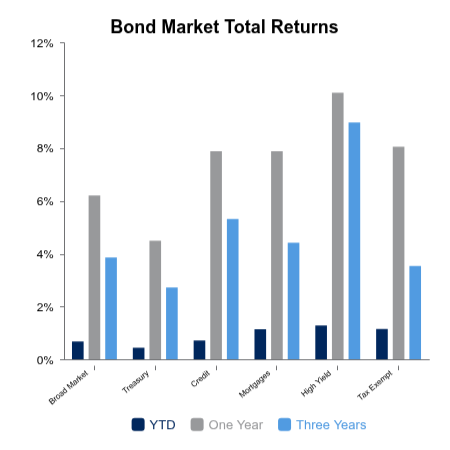

Fixed income markets exhibited negligible price movement over the past week, with broad bond indices advancing a marginal 0.12%, suggesting a transition to a “carry-dominated” environment where investor returns are derived primarily from coupon collection rather than capital appreciation. The benchmark 10-year U.S. Treasury yield remained steady at 4.31%, holding within its recent trading range of 4.20% to 4.40% despite intermittent volatility. The lack of significant price movement underscores a market trying to balance conflicting signals on direction and duration of higher energy costs.

On the back of robust earnings reports, corporate credit spreads continued to slowly compress, with investment-grade bonds currently offering less than 100 basis points (1%) in premium over maturity equivalent U.S. Treasurys.

U.S. retail activity in March 2026 displayed unexpected resilience, with headline sales recording their most significant monthly increase in over a year, driven primarily by an energy-induced price surge and, to a lesser extent, underlying consumer demand. According to the Department of Commerce, total nominal retail purchases rose 1.7% in March, surpassing expectations and following an upwardly revised 0.7% expansion in February. Despite the concentration of spending on fuel, the report indicates broad-based consumer demand, with 12 of 13 retail categories reporting growth. Solid “Core” Sales, excluding the volatile energy category, advanced 0.6%, but inflation adjustments show that real consumer spending was essentially unchanged.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.