Markets Chop Amid Dispersion

- Small caps power ahead.

- Technology shares churn.

- Space stocks come back to earth.

The S&P 500 finished the week down 0.8% with weakness driven by the technology sector. The high-flying KOPSI Index in Korea took a 10% hit on Tuesday, which led to 4% declines domestically in the technology sector. Dispersion is a key theme in the markets in recent weeks. New 52-week highs and new 52-week lows both recorded a level over 1.5% among issues on the New York Stock Exchange. It was the first such occurrence since February of this year, which happened to precede the 9% correction in markets.

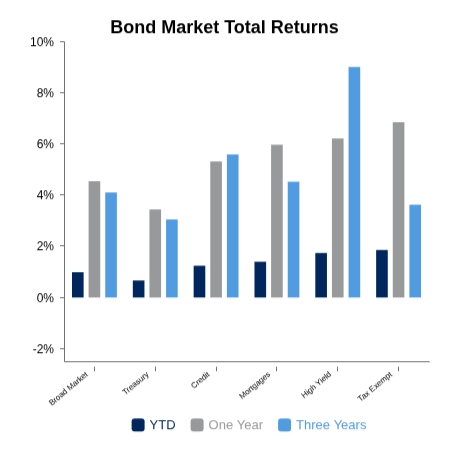

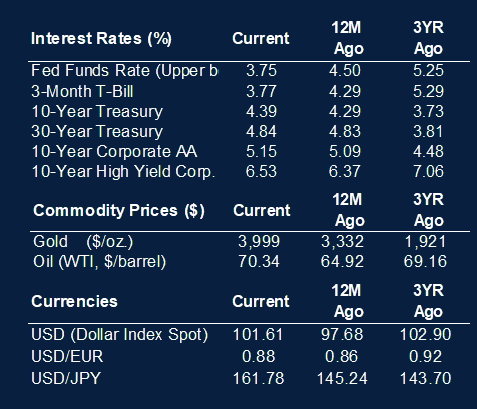

Energy continues to lag with oil prices dipping under $70 per barrel. Yields moved lower on the week, which combined with lower oil prices, helped stage a rally in some homebuilder and consumer names. Amid the technology weakness, the biotech industry had an exceptional week. They recorded their largest 5 day gain relative to the NASDAQ Index in four years.

The space theme is taking a sizeable drawdown following the run-up to the SpaceX IPO. The Tema Space Innovators ETF (NASA) debuted in March to get ahead of the IPO. The ETF rallied 75% in just over a month but has now fallen 37% in just over three weeks. The 50% spike in SpaceX following its open has disappeared, but the stock is holding near its initial opening price as peers move noticeably lower.

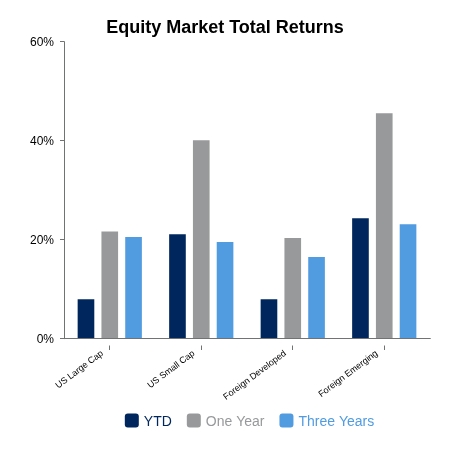

Under the surface, the Russell 2000 continues to perform well. The Russell 2000 reached a new all-time high this week despite the NASDAQ being down more than 5%. Small caps have outpaced the NASDAQ by a sizeable 15% over the last 12 months. Small cap technology and hardware names have done especially well. Telecommunications, Health Care, and Renewable Energy Industry groups are all up more than 50% over the last year.

Economic data remains on pace

The Citi Surprise Index continues to hover near a 3-year high as the economic data comes in better than expected. GDP nowcasts sit around 3% and combined with 3% inflation nets to a nominal GDP running in the 6% area. This is clear of the above 25-year average of 4.6%.

This week saw the S&P 500 US Manufacturing PMI hit a three-year high. The labor market looks to be on solid footing. Jobless claims continue to reside near all-time lows. ADP weekly employment data suggests a potential acceleration in employment.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.