Equities Begin the Year with Strong Gains

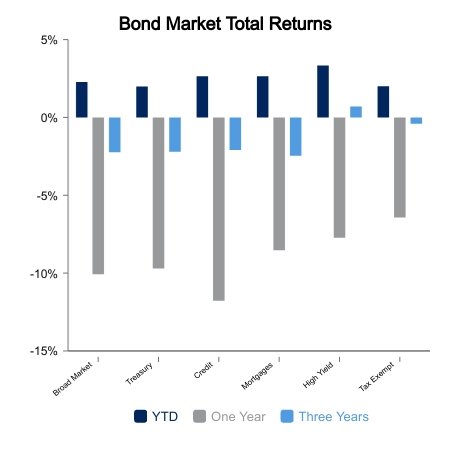

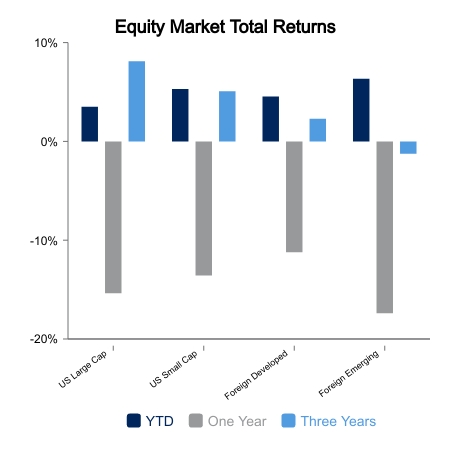

After a weak ending in 2022, equity markets are off to a good start in 2023. The S&P 500 is up 3.4% to begin the year while the NASDAQ and Russell 2000 are both up about 4.5%. Emerging markets are up an even stronger 6.3% as a lower U.S. dollar and falling yields are viewed in a favorable fashion. Core bonds begin the year with a gain of 2.3%.

Optimism for Soft Landing Grows

Despite the rare soft landing in our economic history, this view has taken a major step forward after just a few recent economic releases. Most assets are starting to incorporate this into their current pricing.

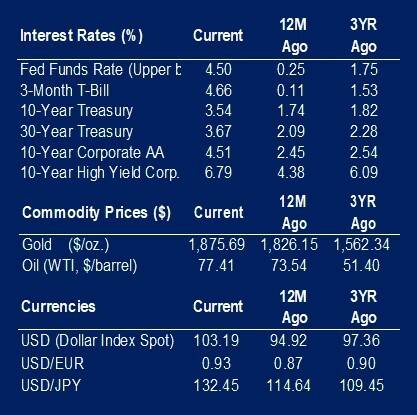

- Corporate credit spreads are at their tightest levels in more than eight months.

- According to FactSet, earnings estimates for fourth quarter 2022, to be reported in the coming weeks, fell 6.5% from Sept. 30 to Dec. 31. This is above the five-year average decline of 2.5%.

- Estimates for fiscal year 2023 fell 4.4% in the period, above the five-year average decline of 0.2%.

- Despite this, the S&P 500 is up more than 10% since the end of September.

The Bureau of Labor Statistics reported that 223,000 net jobs were created in December. This was right in line with expectations and was deemed a golden report of not too hot or cold. The market cheered the fact that average hourly earnings are falling, now at 4.6% versus the prior year. This is down from the 5.6% peak of 2022. Two of the targets for the Fed are to generate falling wages and tighter financial conditions via falling asset prices. They appear to be winning the inflation front on wages and core goods are also deflating at a sharp rate in the last three to four months. However, the market is moving higher and is frequently a talking point as Fed officials don’t appear happy about rising asset prices.

Other economic data reports for the week were quite soft. The ISM Manufacturing report came in at 48.4, a cycle low. The internals were worse as new orders printed 45.2. The normally strong services sector took a spill. The ISM Services Index went from 56.5 to 49.6 over the last month and new orders fell in stunning fashion, from 56.0 in November to 45.2 in December. ISM Services new orders have never reached this level without a recession. It is another data series in a long list that coincides with a recession or more equity weakness. In addition, there is a growing list of things taking place that have never happened outside of a new bull market.

|

|

Source: BTC Capital Management, Bloomberg LP, FactSet, Refinitiv (an LSEG company).

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.