United States Economy Continues Its Resilience

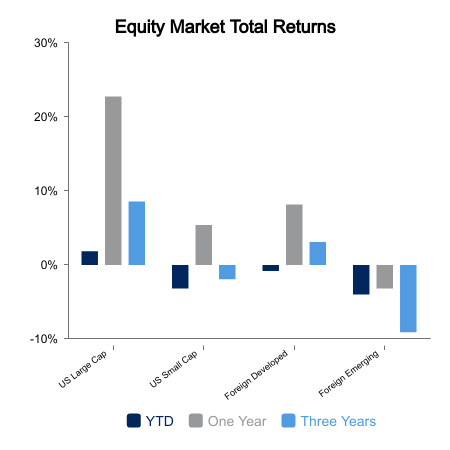

After a negative performance last week, equities retuned to the plus side in a meaningful way this week. The Russell 3000 Index of domestic stocks returned 2.1% for the period. The growth component of the index, the Russell 1000 Growth Index, was even more impressive with a return of 3.3%. Helping to propel stocks higher were last year’s two best performing sectors: Information Technology and Communication Services. The leadership of these two sectors is also seen in the year-to-date differential between growth and value indices. The Russell 1000 Growth Index has returned 4.0% year-to-date, while the Russell 1000 Value Index is trailing with a return of -0.7%. Other market segments also moved higher for the week but at a more modest pace. Small cap stocks advanced 1.8% and developed markets outside the United States had an identical return, also registering 1.8%.

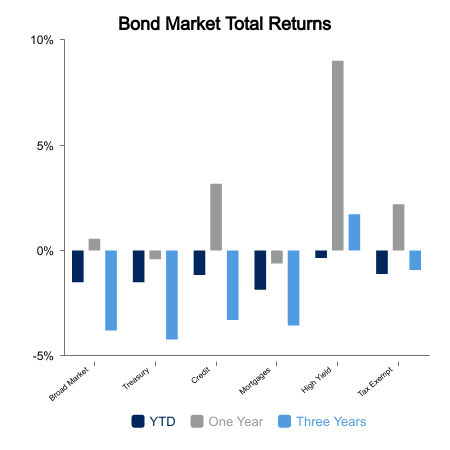

Unlike the equity markets, the bond market did not produce a positive return for the week as it generated a total return of -0.4%. The negative return was attributable to the increase in interest rates that occurred over the period as the yield on the 10-year U.S. Treasury moved from 4.10% to 4.18%.

The economic calendar was relatively light this week but was not without significance. Housing related data was one of the prominent areas represented in this week’s data, with housing starts and building permits both producing better than expected results. Housing starts actually declined month-over-month, but the decrease was less than forecast and the seasonally adjusted annualized rate for the metric was higher. On the negative side, existing home sales were slightly behind the results anticipated by economists.

While the housing data was somewhat mixed, the consumer continued to show strength as the University of Michigan Consumer Sentiment Index registered a much stronger than expected preliminary reading of 78.8. This compares to the forecast of 69.5 and a prior reading of 69.7. The index is now at its highest level since July 2021 and the two-month move is the largest since 1991. Increased confidence that inflation is moderating was a driver of the strong reading, as well as recent gains in the stock market.

Other significant economic data points for the week were the preliminary readings for the Markit PMI series. All three metrics (composite, manufacturing and services) had readings over the 50.0 threshold, which suggests economic growth. Most significant was the result for the manufacturing sector, which was forecast to deliver a reading of 47.8 but delivered a meaningfully stronger result of 50.3.

|

|

Sources: BTC Capital Management, FactSet Research Systems

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.