Happy New Year!

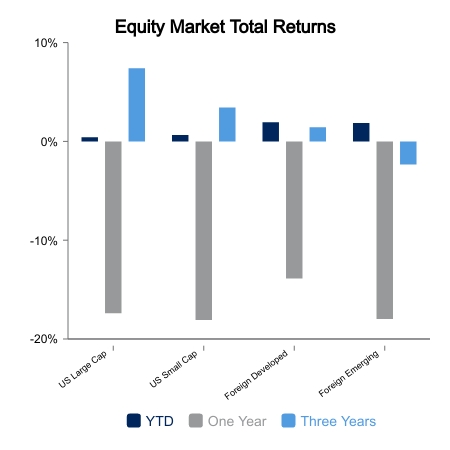

Asset class returns have exhibited a welcome respite from that of 2022. Bonds have rallied 1.1% over the last week as interest rates have declined. U.S. and foreign equities have also exhibited positive returns of 2.1% and 2.0%, respectively. Value continues to outperform growth. While some may attribute this to the Santa Claus rally, investor sentiment may reflect the opinion that peak inflation is in the past and the Fed may need to pivot.

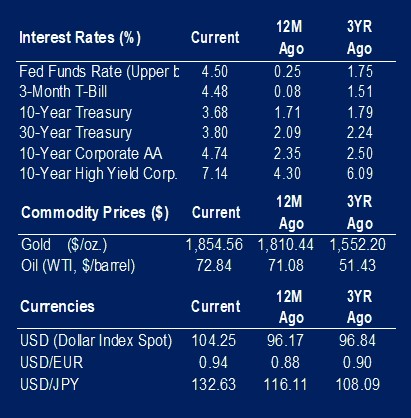

Per the minutes of the Federal Open Market Committee’s meeting of Dec. 14, 2022, “Recent indicators point to modest growth in spending and production. Job gains have been robust in recent months, and the unemployment rate has remained low.” This aspect of modest growth, coupled with stable employment, has been a sustaining factor of the U.S. economy.

This week IHS Markit released its final Purchasing Manager Composite Index report for December, which exhibited modestly positive signs. Recall that a reading above 50 indicates expansion while below 50 indicates contraction. Within the U.S., the index surprised to the upside with a reading of 45.0 versus expectations of 44.6 which was also the reading for November. Outside the U.S., the Eurozone Index came in at 49.3 versus expectations of 48.8, also better than November. Services, which are a greater component than manufacturing, all appeared to exceed November’s reports for all regions. While still below 50, the change in trend is critical as we navigate through 2023. Additionally, the Manufacturing component of the index for December for developed regions and most emerging regions trended upward versus November’s print.

The unemployment report for December will be released on Friday. With that will be non-farm payrolls and earnings. With inflation having declined off its highs seen in 2022, companies may see some relief on margins as the cost of labor may be restrained in the face of declining inflation. More so, certain technology companies have announced layoffs which will also come into play.

Thus, the Fed may be in position to pivot, or at least moderate its interest rate policy as it did in December. According to FactSet, currently the Fed is anticipated to modify its Federal Funds range from 425-450 basis points to 450-475 basis points. One key consideration is the Fed’s own admission that risks appear to be tilted toward weaker inflation and possible recession. If true, the market will continue to price fewer rate hikes followed by earlier rate cuts.

We will be kicking off earnings reports next week for the fourth quarter of 2022. Stay tuned.

|

|

Source: BTC Capital Management, Bloomberg LP, FactSet, Refinitiv (an LSEG company).

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.