Financial Markets Close Out Strong Quarter

- First quarter GDP exceeds expectations.

- Labor market stability continues.

- Consumer resilience continues.

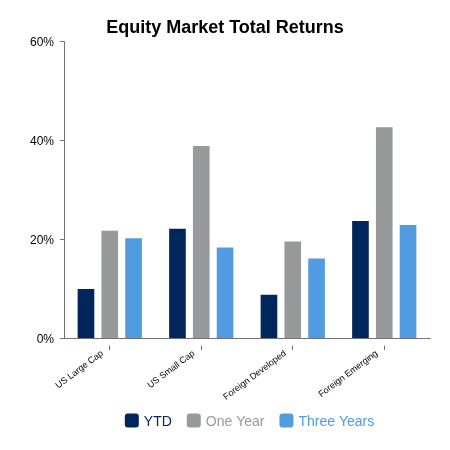

As the United States prepares to celebrate its semiquincentennial, investors already received an early gift from the equity markets as the Russell 3000 Index of domestic companies delivered a second quarter return of 15.4%. This return was the strongest quarterly result in six years and offset the negative performance of -4.7% generated in the first quarter.

For the week, equities continued to deliver positive returns with the Russell 3000 Index returning 1.8%. Growth stocks outperformed their value counterparts but continue to lag on a year-to-date basis. International equities were also positive as the MSCI ACWI ex U.S. Index exhibited a total return of 0.4% for the week and has delivered a strong return of 13.7% year to date.

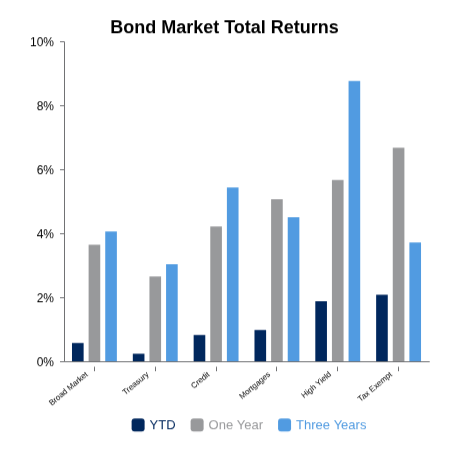

Fixed income provided a return of -0.4% for the week as interest rates rose. The 10-year U.S. Treasury saw its yield rise to 4.48% from the prior week’s level of 4.39%. Despite the negative weekly return, the bond market provided a positive return of 0.7% for the second quarter.

Headlining economic data for the week was the final assessment of first quarter real GDP. Its reading of 2.1% was meaningfully higher than the estimated increase of 1.6%. Interestingly, the contribution from the consumer was lower in this final estimate for the first quarter but its decline was offset by a lower level of imports than had previously been reported. Currently, GDP is forecast to show a growth rate of 2.5% for the second quarter.

Employment data continued to indicate stability in the labor market. Initial and continuing claims for unemployment continue to register modest readings and the JOLTS survey which assesses the level of job openings came in at a higher than forecast level of 7.6 million. This was higher than forecast and represented the strongest reading in two years.

Also released this week was the current reading for the PCE Deflator. This included results for the Core PCE Deflator, the Federal Reserve’s preferred measure of inflation which excludes changes in food and energy prices. For the month of May the figure rose 0.3% and year to date it has increased 3.4%. This is the highest level for the core measure since October 2023.

And finally, we have previously shared comments on the resilience of the U.S. consumer, and this resilience continues to be reflected in the light vehicle (cars, SUVs, minivans and pick-ups) sales data for the month of May which registered 16.1 million units. After dipping down to 14.6 million units in January, the measure has stayed above the 16.0 million level consistently since March.

|

|

Sources: BTC Capital Management, FactSet Research Systems Inc., Federal Open Market Committee (Federal Reserve) LSEG I/B/E/S, FTSE Russell (an LSEG Group company), S&P Global, U.S. Bureau of Labor Statistics, U.S. Census Bureau

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.