Global Equities Remain Resilient

Key Takeaways

- The rise in global equities is driven primarily by earnings growth.

- Macro appears to support equity investor sentiment.

The rise in global equities is driven primarily by earnings growth

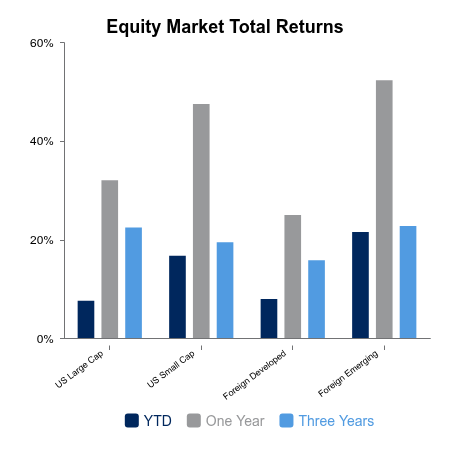

Equities continued to advance over the last week, as multiple domestic and foreign indexes hit new all-time highs driven by strong earnings reports, specifically from technology-related companies. For the week, the Russell 3000 Index rose 3.3%, driven by a 5.4% rise in the Russell 2000 Index (a broad measure of domestic small-cap companies), while the Russell 1000 (a measure of domestic large-cap companies) advanced 3.2%. Returns outside the U.S. were impressive as the MSCI All-Country World Index ex-USA (MSCI ACWI x-USA) rose 3.8% paced by the 5.1% rise in the MSCI Emerging Markets Index and further abetted by the 3.3% advance in foreign developed as exhibited in the MSCI EAFE Index.

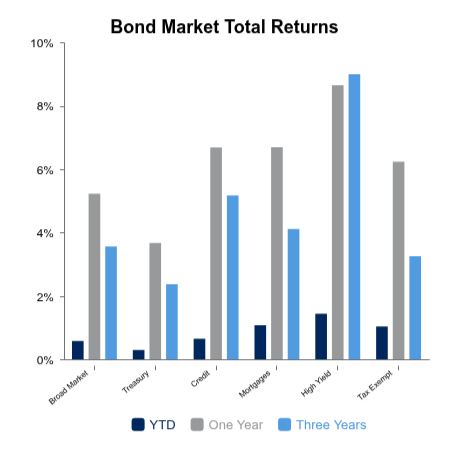

Bonds rose 0.6% for the week given a modest decline in yields.

First-quarter earnings season has been a pleasant surprise. According to LSEG I/B/E/S, 420 of the 535 companies comprising the MSCI USA Investable Market Index (a broad measure of domestic large, mid, and small cap companies) have reported growth in earnings-per-share (EPS) of 25.9% year-over-year (YOY), beating analyst estimates by 8.4%, on average. Analysts currently project EPS growth for this index of 24.6% for the forward 12 months.

For companies outside the U.S., EPS growth for the first quarter has also exceeded expectations. 656 companies of the 1,268 constituents of the MSCI ACWI ex-USA Index, which comprises both foreign and emerging markets, have reported YOY growth in EPS of 26.5%. Analysts currently project EPS growth for this index of 25.7% for the forward 12 months.

Macro appears to support equity investor sentiment

Positive equity sentiment appears to be driven by other factors. Last Thursday, the Bureau of Economic Analysis (BEA) released its first of three estimates of U.S. Gross Domestic Product (GDP) for the first quarter of 2026. BEA reported real gross domestic product (GDP) increased at an annual rate of 2.0%, versus 0.5% for the fourth quarter of 2025. Contributors to this rise were investment, exports, consumer spending, and government spending while imports, which are a subtraction in the calculation of GDP, increased.

A pause in the U.S. – Iran conflict also contributed to positive sentiment. Oil prices, having hit four-year highs, began to descend. Concerns about inflation may have abated, in the near term, enabling the Fed to stay on the sidelines.

Never a dull moment (or market).

|

|

Sources: BTC Capital Management, FactSet Research Systems, Inc., LSEG I/B/E/S, FTSE Russell (an LSEG Company), MSCI Inc., Bureau of Economic Analysis.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.