Happy New Year!

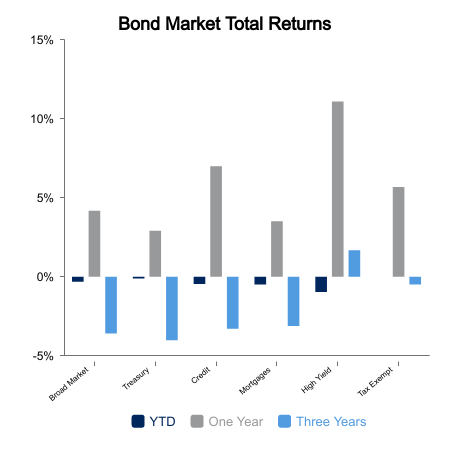

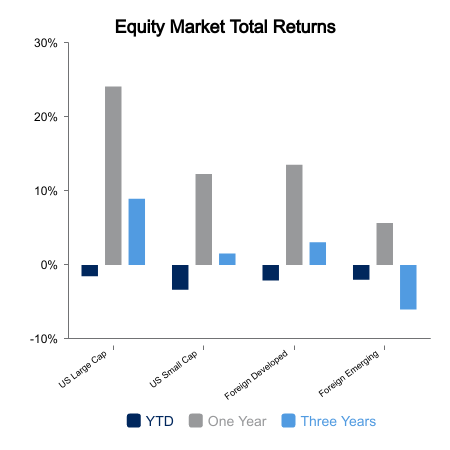

Equities finished lower for the week due to a “risk-off” mentality in the markets, reversing the trend from the prior week. The S&P 500 finished down 1.6%, while the Nasdaq was down 3.4%. Small caps experienced a more significant sell-off, falling 4.5%. Treasury yields backed up during the week, off of their five-month lows, with bond indices falling 0.9%. The Magnificent 7, which has dominated stock market headlines for the better part of a year, underperformed the broader markets.

“Soft Landing” for 2024?

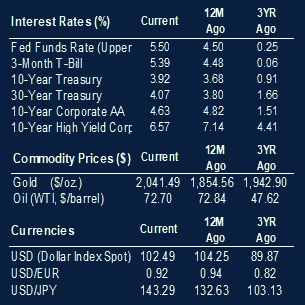

Investors are anticipating a “soft landing” with regards to the Federal Reserve’s policies. In their December meeting, Federal Reserve officials viewed the policy rate as likely at or near its peak for this tightening cycle. They stated a lower target range for rates would be appropriate by the end of 2024, citing declining inflation rates and a more robust supply chain. However, there remains uncertainty as to the timing of rate cuts during the year.

IHS Markit released its final Manufacturing Index Report for December, coming in slightly lower than expected at 47.9 (a value under 50 indicates a contraction in activity, whereas a value over 50 indicates expansion). The Manufacturing Index has been at or below 50 for 15 consecutive months. However, manufacturing is a significantly lower proportion of the economy versus the services segment of the economy, which continued to exhibit strength for most of 2023.

The JOLTS job openings for November came in higher than expected. Although the figure was at its lowest level since April 2020, it is still well above its 10-year average as the labor market continues to exhibit consistent strength, despite continued, though muted, fears of an upcoming recession. Later this week, the non-farm payrolls and unemployment rate for December will be released, and undoubtedly investors will be watching these figures to see if there are any signs of weakness in a generally strong labor market.

Stock Market Optimism Continues

Investors are generally upbeat regarding their view on the equity markets following a very strong 2023. The AAII U.S. Investor Sentiment Index measures the difference between the percent of investors who are currently bullish on the market versus the percent of investors who are bearish on the market. The Index is currently at the high end of its 10-year range indicating there is much optimism regarding the stock market.

There are however lingering fears regarding a potential recession as economists have recently noted an increased movement in negative economic growth indicators, which may lead to instability in corporate and personal spending, as well as cutbacks in the labor market. It is important to note that many predictive economic leading indicators have been incorrect since 2020 given the extreme and unprecedented events that transpired during and after the pandemic.

|

|

Sources: BTC Capital Management, S&P Dow Jones Indices, IHS Markit, Factset, American Association of Individual Investors

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.