June’s unemployment rate was better than expected despite a resurgence of COVID-19 cases in some states. 11.1% of the U.S. labor force remains unemployed. The rate, a significant increase from last year, is lower than the consensus’ estimate of 12.5%. May’s reading was at 13.3%. The report showed a reduction in the number of people who had been temporarily laid off. However, there was an increase in the number of people who have lost their jobs permanently. Unfortunately, we are seeing an increase in the number of companies unable to make it through the reduction in demand induced by COVID-19. Despite the better than expected employment picture, initial unemployment claims were higher than expected with 1.427 million people filing for unemployment insurance. This number is in line with last month’s initial claims number of 1.482 million but higher than the expected 1.350 million.

Year-over-year growth in earnings continues to be strong. As discussed in previous weeks, the number is skewed toward higher wage workers since the layoffs impacted lower wage workers the most. Earnings grew by 5% in June. Month-over-month growth tells a different story. In June, earnings decreased by 1.2%. This number is probably impacted by more people re-entering the work force, reducing the average total wage number.

A recent bright spot for the economy has been manufacturing. Manufacturing payrolls increased to 356,000. This compares with the expected number of 235,000 and last month’s reading of 250,000. Company inventories have been depleted. The pickup may reflect manufacturing companies ramping up production to supply depleted inventory.

The final Durable Orders numbers for May were released this week. Ordering grew by 15.7%. The increase was led by orders for transportation equipment. After two consecutive months of decreases, transportation equipment orders increased by 80.7% in May.

We are at the start of another earnings season. Expectations for the second quarter are low. The quarter is expected to feel the full brunt of COVID-19. S&P 500 earnings are expected to decline by 43.9% and sales are expected to be down 11.6%. The negative growth is expected to continue into the third and fourth quarters.

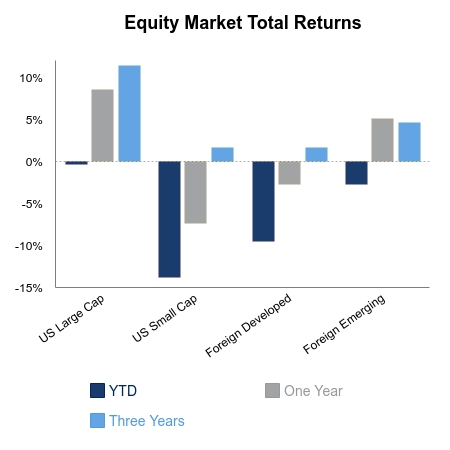

Over the one-week period, the S&P 500 was up 1.76%. The positive return was led by sectors that have been relatively strong through the year, including consumer discretionary, information technology and communication services.

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.