Softening in the Housing Market

There was a little more softening in the housing market this week. April existing home sales were down 2.4% from March. The sales of 5.61 million, however, were slightly higher than the expected 5.6 million. According to the National Association of Realtors, higher home prices and higher mortgage rates have negatively impacted buyer activity. Housing inventory is up 10.8% from March to 2.2% this month but is still 10.4% lower than a year ago. We’re seeing supply slowly increasing.

Sales of new homes were significantly lower than expected in April. Only 591,000 new homes were sold compared to the expectation of 750,000. In March, 709,000 were sold. The month-over-month drop of 16.6% is the biggest decrease since 2013. However, the decrease in housing sales has not led to a decline in home prices. Home prices are still high with the median price in April at $450,600. This is a 19.6% increase from a year ago. The average sales price is $570,300.

The Conference Boards’ Leading Economic Index declines

- The Conference Board’s Leading Economic Index declined by 0.3% in April.

- The decline was attributed to weak consumer expectations and a drop in residential building permits.

- The index is designed to signal peaks and troughs in the business cycle.

May PMI Numbers

Preliminary Purchasing Managers’ Index (PMI) numbers are out for May. Manufacturing PMI was down to 57.5 from 59.2 last year. Services PMI was also lower at 53.5 compared to the previous month’s 55.6. The decreases are concerning but not alarming. PMI readings over 50 are considered positive.

Durable Good Orders Increased in April

Durable goods orders increased by 0.4% in April. The increase contributes to the index being up six out of the last seven months. The rise was led by increases in transportation equipment. The increase is lower than the previous month and expected increase of 0.6%. Excluding transportation equipment, durable goods orders are up 0.3%.

Earnings Season Update

Earnings reports continued to trickle in this week, and now 97% of S&P 500 companies have reported. Earnings are up 9.4%, which is 4.8% better than expected. Growth in earnings has been led by the Energy and Materials sectors. The Consumer Discretionary and Financials sectors are the only two sectors with negative growth, down 33% and 20% respectively. Sales are up 13.8% for the first quarter. This is 2.6% better than expected and growth here is also led by Energy and Materials. Every sector saw growth in sales in the first quarter.

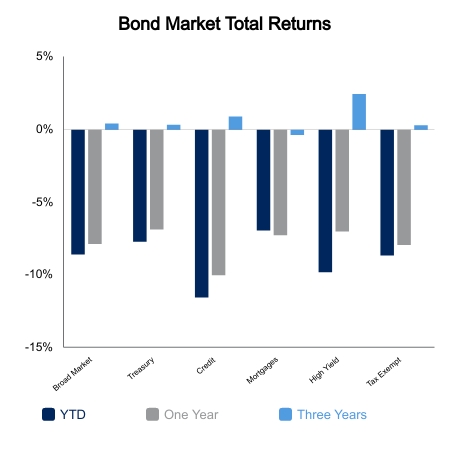

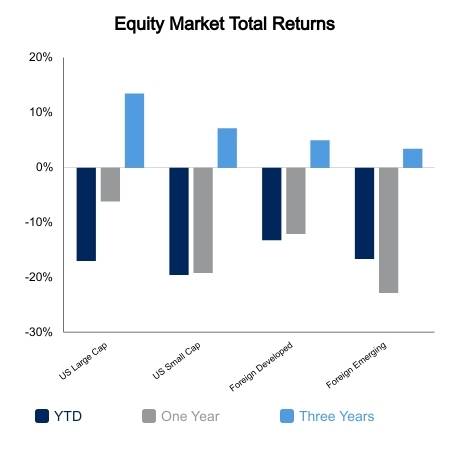

|

|

Source: BTC Capital Management, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.