Retail sales in October were the highest they have ever been. The increase of 1.7% outpaced the expected increase of 1.2%. The largest increase of 4% came from non-store retailers. Electronics and appliance stores also saw sharp increases in purchases with a rise of 3.8%. As we approach the holiday season, high demand is not expected to aid in easing supply chain issues. Large retail companies have indicated they are prepared for high demand as holiday gift buying begins.

Companies continue to struggle filling positions. The Job Openings and Labor Turnover Survey results from September showed 10.438 million open jobs. This is down from last month’s 10.629 million but significantly higher than the 10-year average of 5.8 million. Low labor force participation numbers have contributed to the large number of openings. Market participants have started to doubt that labor force participation will approach pre-pandemic levels any time soon. However, unemployment is expected to continue to decrease through 2022.

Preliminary results for November show that consumer sentiment is lower than in October according to the University of Michigan. The reading of 66.8 compares unfavorably with last month’s 71.7. The 6.8% dip has been attributed to inflation fears. The survey shows that one in four consumers referenced lower living standards in November due to inflation. Negative real wage growth has contributed to consumers being able to purchase less than they did a year ago.

Business inventories were up 0.70% in September. The reading, which is 0.10% better than expected, is indicative of companies building inventories. A build up in inventories is usually associated with a positive economic outlook and is considered a leading indicator.

Earnings season comes to a close with 95% of S&P 500 companies reporting. Earnings are up 40.74% over last year. This high growth number is 10.20% better than expected. The Information Technology sector contributed the most to the growth in earnings. Performance in Energy and Financials were also a strong contributor. Revenue was up 18.25% in the quarter, 2.82% better than expected. The Energy and Health Care sectors were the largest contributors here. Double digit earnings and sales growth are expected to continue through the fourth quarter.

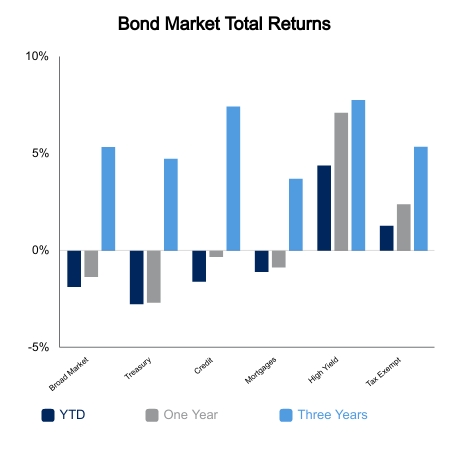

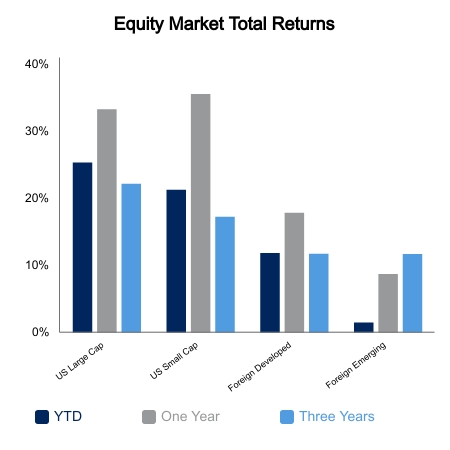

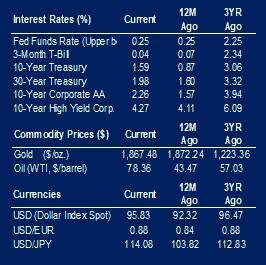

|

|

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.