Employment data dominated the economic releases for the week as the unemployment rate ticked higher to 3.9%, the highest level since January 2022. Also, the increase in non-farm payrolls registered 150,000, below the anticipated increase of 180,000. Not only was the monthly increase lower than expected, but revisions were also made to the results for the prior two months which reduced totals for those months by 101,000. Across private sector industries only 52.0% reported increased levels of employment which is the lowest since April 2020. This month’s employment report was negatively impacted by the UAW strike in place against domestic auto manufacturers.

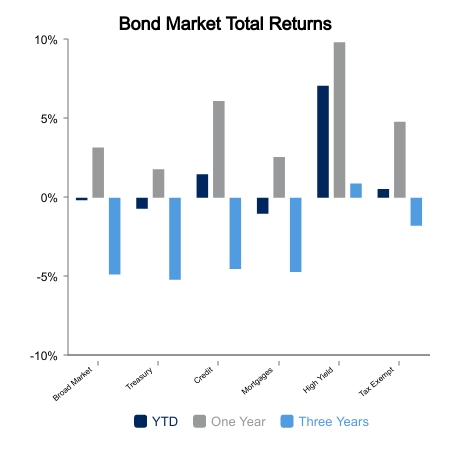

The moderation in the employment data was a significant boost to the spirits of investors as they interpreted the results as further support for the Federal Reserve ending increases to the Fed Funds rate and potentially starting the process of reducing the rate. Both stocks and bonds were beneficiaries of the improved mood. The 10-year Treasury saw its yield decline from 4.7% to 4.5% which translated into a weekly return of 1.7% for broad bond market indices. Bonds have now improved to the point where their total return is virtually flat on a year-to-date basis coming in at -0.2%.

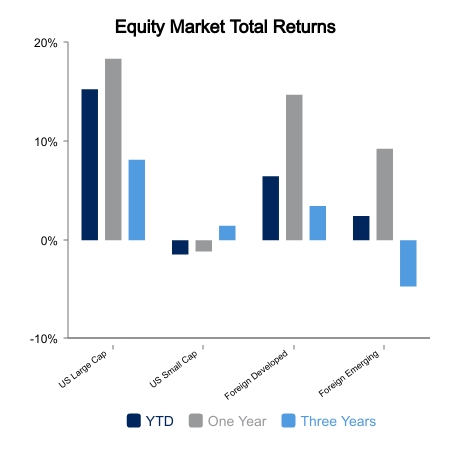

Equities experienced even better returns for the week as major indices in the U.S. saw very strong returns. For example, the Russell 3000 Index of domestic equities returned 4.5% while the growth segment, as measured by the Russell 1000 Growth Index, delivered a robust 6.4% return. International markets also rose but at a more modest pace with the MSCI EAFE Index registering a return of 1.4%. Also contributing to enthusiasm in the equity markets were the better-than-expected results from third quarter earnings reports. For Standard & Poor’s 500 Index component companies the current expectation is a year-over-year increase of 3.7% for the quarter. If this level of growth actually transpires it will be the first quarter of positive year-over-year growth since the third quarter of 2022.

Next week’s economic releases will include updated figures for the Consumer and Producer Price Indices. A potential positive contributor to further inflation data moderation is continued progress on the labor front, as recent employment related data revealed easing in year-over-year and month-over-month hourly earnings increases. Combining this with a declining oil price could help the inflation rate to show further moderation. For perspective, the price of oil has fallen approximately 20% since its most recent peak of $93.68 per barrel on September 27.

|

|

Source: BTC Capital Management

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.