Consumer Focused Data Week

With consumers representing almost 70% of the gross domestic product (GDP) in the U.S., this week’s economic news gave us a picture of how they are doing. A reading on the job outlook showed mixed signals. While headline nonfarm payroll (Current Employment Statistics) increased by 261,000 in October (vs. 315,000 in September), the household survey (Current Population Survey) painted a vastly different picture. According to the household survey unemployment rose by 306,000 in October versus a prior month drop of 261,000. This increase is what pushed the unemployment rate to 3.7% according to the Bureau of Labor Statistics. These two measures differ in how they evaluate employment so are used together to provide a full picture of the labor market.

The next set of consumer-focused data was take-home pay. While working an average of 34.5 hours weekly in October, about 20 minutes less than a year ago, Average Hourly Earnings were up 0.3% for the month of October and 4.7% over the last 12 months. Reports suggest demand for workers remains robust despite efforts by monetary authorities to slow the pace of economic growth. Layoffs, while rising, remain low by historical standards. The recent Challenger, Gray & Christmas survey revealed more job cut activity is anticipated in the fourth quarter as companies finalize budgets and plans for 2023.

Small Business Outlook

A major factor of job growth has been U.S. small businesses. Adding to the mixed signals in the employment picture was a recent NFIB Small Business Optimism Index, that fell to 91.3 from 92.1 as seven of the gauge’s 10 components declined. The decline was led by both a retreat in sales expectations and in the number of firms planning to hire. This survey also reported inflation as the number one concern of the respondents, yet only 50% of the owners felt confident that they can increase prices in the current environment. They are also anticipating that future earnings will be lower due to margin pressures.

Election – Stability of Gridlock

Equity markets as of the close on Wednesday are up +1.7% for the week according to the MSCI USA Index. This result provides a major contribution to the one-month tally of +2.1%. Election results show a divided government that, from a rearview mirror perspective, is good for investors. Historically, a Republican congress under a Democratic president has been the strongest environment for stocks. Measured one year following the last 19 midterm elections since World War II, the S&P 500 has averaged a return of +14.4%, according to Bespoke Investment Group. In every instance the return for the one-year period following the midterms has been positive.

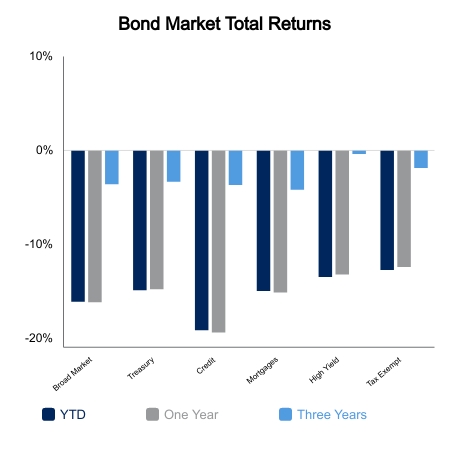

|

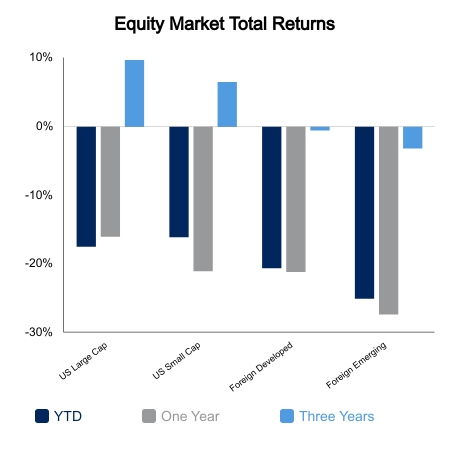

|

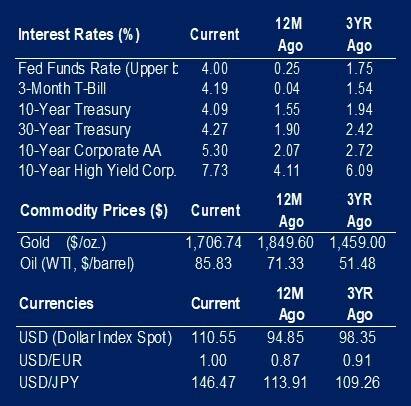

Source: BTC Capital Management, Ibbotson Associates, FactSet, Refinitiv.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

This content is provided for informational purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and should not be interpreted as investment, tax, legal, and/or financial planning advice. All investments involve risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.