The economy is still growing. It looks like we can push recession fears back at least another two quarters. That is, if you define recession as a fall in GDP over two successive quarters. GDP growth in the third quarter came in at 1.9%. Some market participants were disappointed with this number, despite it being better than the expected 1.7%. Sometimes, it seems like investors enjoy the thorns much more than the roses. The 1.9% is more in-line with long term sustained growth than the 3% we saw in the second quarter of 2018. This growth was led by consumer and government spending, residential investments and exports. However, it wasn’t all rosy. Consumer spending growth slowed from the previous quarter. Personal consumption expenditure grew by 1.5% in the third quarter. This compares with growth of 2.4% in the second quarter. Business investment continues to be a drag on economic growth.

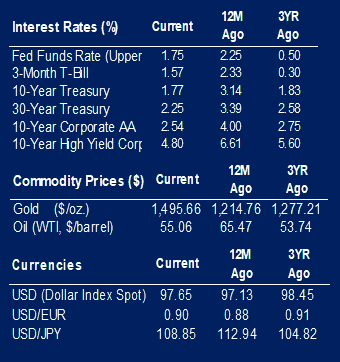

On Wednesday, the Federal Reserve (Fed) announced a cut to the benchmark federal funds rate. The cut was by 25 basis points, putting the rate between 1.50% and 1.75%. This is the third time the Fed has cut rates this year. Although, the Fed has signaled future rate cuts are not imminent. The indication from Federal Reserve Chair, Jerome Powell, is that it will take a significant downward shift in economic growth to justify another cut. Money may be getting less easy.

Durable goods orders took a bit of a tumble as manufacturing pressures continue to negatively impact purchasing. Orders were down 1.1% in September. This is lower than the expected contraction of 0.55% and the previous month’s growth of 0.3%. Fewer transportation equipment orders led the decrease. Excluding transportation, orders were down 0.3%.

We saw some strength in manufacturing this week. The Preliminary Markit PMI manufacturing number for October was 51.5. The expectation was for a reading of 50.6.

Consumer optimism dipped slightly in October, as measured by the Michigan Sentiment Index and the Conference Board’s Consumer Confidence Index. Readings for both were 95.5 and 125.9 respectively. This is lower than the expected 96 and 127.8. However, these numbers are still strong.

There’s also some strength on the home front. New home sales were up 701,000, which is 1,000 better than expected. Pending home sales grew by 1.5% over the previous month, which is higher than the anticipated 0.95%. Requests for building permits were 4,000 higher than expected at 1,391,000.

|

|

Contributed by | Kuuku Saah, CFA, Investment Analyst

Kuuku is an Investment Analyst at BTC Capital Management with nine years of investment management experience. Kuuku’s primary responsibilities include portfolio management and analysis. Kuuku attended Drake University and double-majored in finance and economics. He is a holder of the right to use the Chartered Financial Analyst® designation.

Source: BTC Capital Management, Bloomberg LP, Ibbotson Associates, FactSet.

The information provided has been obtained from sources deemed reliable, but BTC Capital Management and its affiliates cannot guarantee accuracy. Past performance is not a guarantee of future returns. Performance over periods exceeding 12 months has been annualized.

The information within this document is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. Statements in this report are based on the views of BTC Capital Management and on information available at the time this report was prepared. Rates are subject to change based on market and/or other conditions without notice. This commentary contains no investment recommendations and you should not interpret the statement in this report as investment, tax, legal, and/or financial planning advice. All investments involved risk, including the possible loss of principal. Investments are not FDIC insured and may lose value.